Stay Ahead in Fast-Growing Economies.

Browse Reports Now

Orthopedic Prosthetic Market Emerging Trends, Challenges & Strategic Forecast (2024-2032)

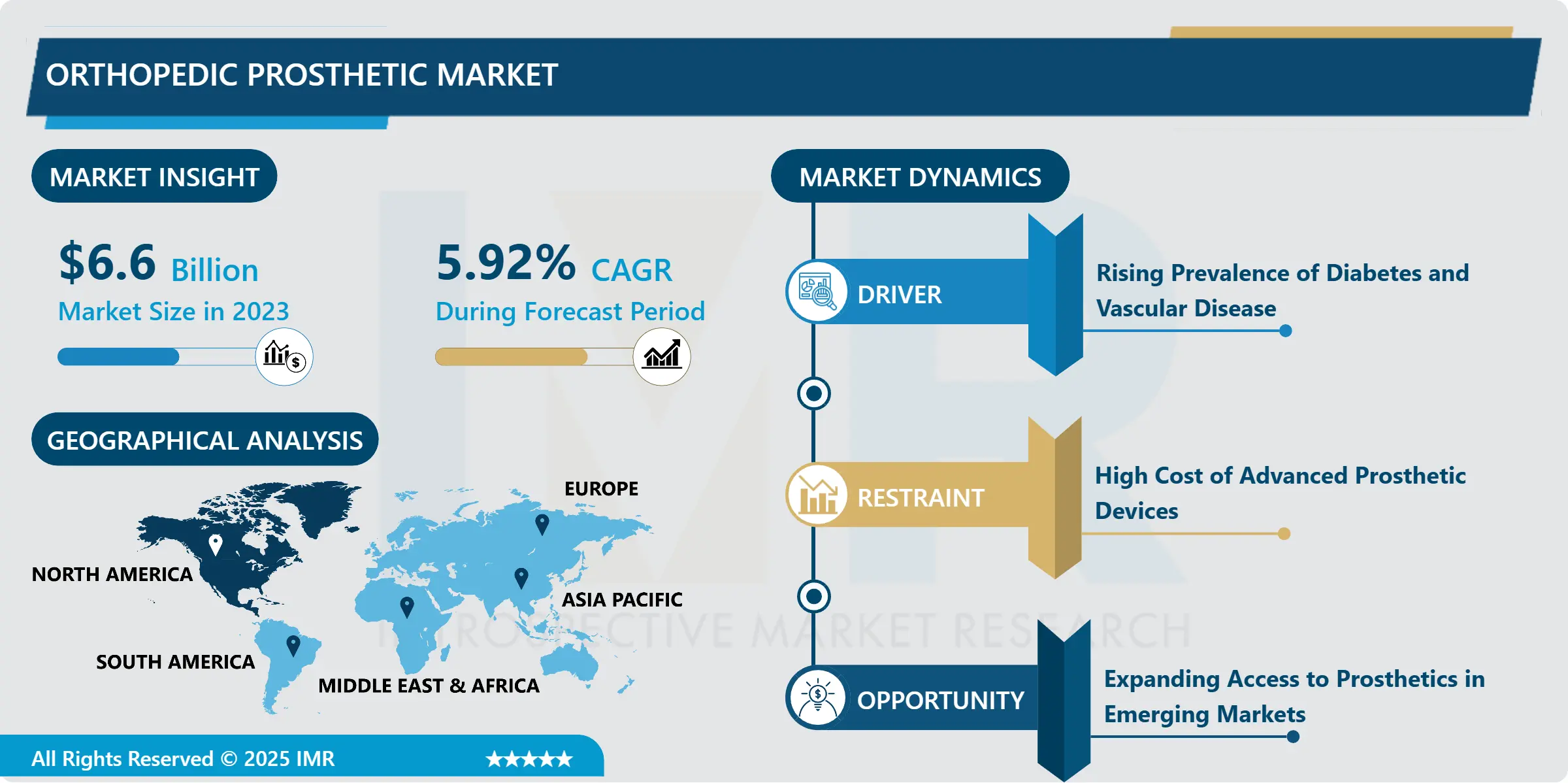

Orthopedic Prosthetic Market Size Was Valued at USD 6.6 Billion in 2023, and is Projected to Reach USD 11.1 Billion by 2032, Growing at a CAGR of 5.92% From 2024-2032. The orthopedic prosthetic market involves the development, manufacturing, and application of artificial devices designed to replace lost or damaged limbs and joints.

IMR Group

Description

Orthopedic Prosthetic Market Synopsis:

Orthopedic Prosthetic Market Size Was Valued at USD 6.6 Billion in 2023, and is Projected to Reach USD 11.1 Billion by 2032, Growing at a CAGR of 5.92% From 2024-2032.

The orthopedic prosthetic market involves the development, manufacturing, and application of artificial devices designed to replace lost or damaged limbs and joints. These prosthetics restore mobility, improve functionality, and enhance quality of life for individuals who have undergone amputations due to trauma, congenital defects, vascular diseases, or diabetes. The market spans both upper and lower extremity prosthetics and includes conventional mechanical devices as well as technologically advanced, sensor-enabled prostheses.

The orthopedic prosthetic market is undergoing rapid transformation, driven by technological innovation and rising patient expectations. Traditionally focused on mechanical replacements for lost limbs, the industry has evolved to incorporate advanced materials, robotics, AI integration, and personalized designs. 3D printing has also revolutionized the field, offering faster, more affordable, and customizable prosthetic solutions. This transition from standardized products to patient-specific devices marks a major shift in the orthopedic landscape.

Population dynamics, especially the aging demographic in developed countries, and a rising incidence of conditions like diabetes and peripheral artery disease are increasing the number of amputations globally. Furthermore, road traffic accidents and battlefield injuries continue to fuel demand for effective prosthetic rehabilitation. In low- and middle-income countries, various NGOs and international health bodies are focusing on increasing access to affordable prosthetic care, further contributing to global market expansion.

Despite growing demand, the market faces several challenges, including high costs of advanced prosthetics, limited trained personnel in remote areas, and reimbursement issues. Nonetheless, continuous innovation, growing investments in R&D, and strategic collaborations between governments and manufacturers are expected to alleviate some of these barriers. The emphasis on functionality, comfort, and aesthetics is pushing manufacturers to create next-generation prosthetics that closely mimic the natural movement and appearance of human limbs.

Orthopedic Prosthetic Market Trend Analysis:

Rising Incidence of Amputations due to Chronic Diseases

A primary factor driving the orthopedic prosthetic market is the global rise in chronic diseases such as diabetes and peripheral artery disease, both of which are leading causes of lower limb amputations. According to the International Diabetes Federation, over 537 million adults were living with diabetes in 2021, and this number is expected to rise to over 643 million by 2030. In severe cases of diabetic foot ulcers, amputation becomes necessary to prevent life-threatening infections. This increases the population in need of reliable and functional prosthetic solutions, especially lower limb prosthetics.

To address the growing limb loss burden, healthcare systems are expanding access to post-amputation rehabilitation and prosthetic devices. The demand for user-friendly, lightweight, and durable prosthetic limbs is encouraging companies to design improved socket systems and dynamic components for active lifestyles. Government programs and insurance schemes in countries such as the U.S., Germany, and Japan are further supporting this growth by covering part or full cost of advanced prosthetic fittings, especially for patients with chronic diseases.

Integration of AI and Robotics in Prosthetics

The integration of artificial intelligence (AI), machine learning, and robotics into prosthetic limbs represents a significant opportunity for industry growth. AI-powered prosthetics can analyze and predict user movement patterns, adapting in real-time to offer seamless motion. Sensors embedded in these devices allow for biofeedback mechanisms that enhance control, stability, and overall functionality. Myoelectric and brain-computer interface (BCI)-enabled limbs are rapidly moving from research labs to commercial availability.

This tech-enabled evolution is attracting investments from both public and private sectors. Governments and research foundations are funding projects that aim to develop prosthetics controlled by neural impulses or that offer haptic feedback to simulate the sense of touch. These innovations also facilitate better integration with mobile health platforms, allowing remote diagnostics and usage monitoring. As manufacturing processes such as 3D printing allow for personalization, AI-based smart prosthetics will continue to gain traction—particularly in urban and high-income markets.

Orthopedic Prosthetic Market Segment Analysis:

Orthopedic Prosthetic Market Segmented based on product Type, Technology, End-User, and Region.

By Product Type, the Lower Extremity Prosthetics segment is expected to dominate the market during the forecast period

Lower extremity prosthetics dominate the market due to their widespread use among patients who have undergone amputations below the hip, knee, or ankle. Common subtypes include transfemoral (above knee), transtibial (below knee), Syme’s, and foot prosthetics. These are designed to restore walking, running, and balancing functions. They are built with advanced composite materials like carbon fiber that combine strength, shock absorption, and light weight—enabling more natural gait cycles and reducing user fatigue.

Functionality enhancements include multi-axial ankles, rotatable knees, and dynamic foot systems to replicate human biomechanics. Modular components provide adaptability, while advanced socket interfaces improve skin compatibility and prevent sores. With the increasing demand from war veterans, accident survivors, and diabetic patients, this segment remains the largest and most essential, particularly in North America and Asia-Pacific regions where amputation rates are high.

By Technology, Electric-powered Prosthetics segment expected to held the largest share

Electric-powered prosthetics, commonly referred to as myoelectric limbs, utilize electrical signals from the user’s remaining muscles to control movement. These devices are highly preferred in upper limb applications—where fine motor control is critical. Sensors detect EMG signals (electromyographic), which are then processed to drive motors in prosthetic hands or arms, enabling precise grip, release, and wrist rotation.

These smart limbs are rapidly gaining traction due to their superior control, functionality, and the increasing availability of battery-efficient designs. They are particularly beneficial for children and working adults requiring enhanced daily life integration. While the initial costs and maintenance are higher, increasing insurance coverage and patient preference for technologically advanced devices have made electric-powered prosthetics one of the fastest-growing segments in the market.

Orthopedic Prosthetic Market Regional Insights:

North America is expected to dominate the Market Over the Forecast period

North America holds a dominant share in the orthopedic prosthetic market and is expected to maintain its lead throughout the forecast period. This dominance is attributed to several factors, including a highly developed healthcare infrastructure, early adoption of innovative technologies, and comprehensive reimbursement frameworks under Medicare, Medicaid, and private insurance plans. The U.S. Department of Veterans Affairs also plays a key role in facilitating access to prosthetics for military personnel.

In addition, the region is home to several leading global prosthetics manufacturers, research institutions, and innovation hubs that actively contribute to the development and testing of next-generation prosthetic limbs. Collaborations between medical centers and technology companies such as Össur and Ottobock North America are facilitating the growth of AI-powered and robotic limbs. High awareness and availability of skilled clinicians further reinforce North America’s market leadership.

Active Key Players in the Orthopedic Prosthetic Market

Aether Biomedical (Poland)

BioMetrics Prosthetic and Orthotic Group (USA)

Bionic Prosthetics and Orthotics Group (USA)

Blatchford Ltd. (UK)

College Park Industries (USA)

Endolite India Ltd. (India)

Exoneural Network AB (Sweden)

Fillauer LLC (USA)

Freedom Innovations (USA)

Medi Prosthetics (India)

Motion Control Inc. (USA)

Össur (Iceland)

Ottobock (Germany)

Protunix (USA)

Reboocon Bionics (Netherlands)

RSLSteeper (UK)

Spinal Technology Inc. (USA)

Steeper Group (UK)

Trulife (Ireland)

WillowWood Global LLC (USA), and Other Active Players.

Key Industry Developments in the Orthopedic Prosthetic Market:

July 2023: With a construction height of little under 5.5 inches and WillowWood’s META-Unibody platform, the Fiberglass META Shock X offers a number of fitting possibilities for different limb lengths. Additionally, it contains an integrated shock unit that combines torsional rotation and vertical impact protection on top of the fiberglass plate.

June 2023: The Myo/One Electrode system, created in collaboration with Coapt, was introduced by Fillauer. It is a compact, waterproof solution that eliminates the need for construction aids, sealing rings, cables, and other devices in favor of a cable. It also provides two EMG signal channels for myoelectric devices through a single preamplifier. The system includes two different ways to connect and works with most dual-site myoelectric devices.

May 2023: In collaboration with Coapt, WillowWood unveiled the Alpha Control Liner System, a cutting-edge prosthetic liner with built-in electronics. The approach benefits users of myoelectric prostheses by allowing for more reliable and pleasant electrode contact with the skin, which improves functional control. To comprehend user intentions and manage prosthetic activities, Coapt’s Complete Control system uses machine learning.

March 2023: Steeper Group stated that it has merged with the Eqwal Group, with the latter purchasing all of Steeper Group’s shares. The Eqwal Group is a multinational provider of prosthetics and orthotics patient care services with its headquarters in Toulouse, France. With this advancement, Steeper Group hopes to improve its healthcare capabilities in the UK and offer cutting-edge goods and services.

January 2023: For its lower limb portfolio, Steeper Group introduced the LIMB-art Prosthetic Leg Covers, which come in distinctive styles and may be customized to boost patients’ confidence and self-esteem. The coverings weigh less than 250 g each and come in 4 models: Core, Vent, Ultralight, and Wave. Additionally, they were created utilizing premium Nylon, which gives the final product strength and flexibility.

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter’s Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Orthopedic Prosthetic Market by Product Type

4.1 Orthopedic Prosthetic Market Snapshot and Growth Engine

4.2 Orthopedic Prosthetic Market Overview

4.3 Upper Extremity Prosthetics

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.3.3 Key Market Trends, Growth Factors and Opportunities

4.3.4 Upper Extremity Prosthetics: Geographic Segmentation Analysis

4.4 Lower Extremity Prosthetics

4.4.1 Introduction and Market Overview

4.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.4.3 Key Market Trends, Growth Factors and Opportunities

4.4.4 Lower Extremity Prosthetics: Geographic Segmentation Analysis

4.5 Socket Prosthetics

4.5.1 Introduction and Market Overview

4.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.5.3 Key Market Trends, Growth Factors and Opportunities

4.5.4 Socket Prosthetics: Geographic Segmentation Analysis

4.6 Modular Components

4.6.1 Introduction and Market Overview

4.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.6.3 Key Market Trends, Growth Factors and Opportunities

4.6.4 Modular Components: Geographic Segmentation Analysis

Chapter 5: Orthopedic Prosthetic Market by Technology

5.1 Orthopedic Prosthetic Market Snapshot and Growth Engine

5.2 Orthopedic Prosthetic Market Overview

5.3 Conventional Prosthetics

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.3.3 Key Market Trends, Growth Factors and Opportunities

5.3.4 Conventional Prosthetics: Geographic Segmentation Analysis

5.4 Electric-powered Prosthetics

5.4.1 Introduction and Market Overview

5.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.4.3 Key Market Trends, Growth Factors and Opportunities

5.4.4 Electric-powered Prosthetics: Geographic Segmentation Analysis

5.5 Hybrid Prosthetics

5.5.1 Introduction and Market Overview

5.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.5.3 Key Market Trends, Growth Factors and Opportunities

5.5.4 Hybrid Prosthetics: Geographic Segmentation Analysis

Chapter 6: Orthopedic Prosthetic Market by End User

6.1 Orthopedic Prosthetic Market Snapshot and Growth Engine

6.2 Orthopedic Prosthetic Market Overview

6.3 Hospitals

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.3.3 Key Market Trends, Growth Factors and Opportunities

6.3.4 Hospitals: Geographic Segmentation Analysis

6.4 Prosthetic Clinics

6.4.1 Introduction and Market Overview

6.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.4.3 Key Market Trends, Growth Factors and Opportunities

6.4.4 Prosthetic Clinics: Geographic Segmentation Analysis

6.5 Rehabilitation Centers

6.5.1 Introduction and Market Overview

6.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.5.3 Key Market Trends, Growth Factors and Opportunities

6.5.4 Rehabilitation Centers: Geographic Segmentation Analysis

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Orthopedic Prosthetic Market Share by Manufacturer (2023)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 ÖSSUR (ICELAND)

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 OTTOBOCK (GERMANY)

7.4 BLATCHFORD GROUP (UNITED KINGDOM)

7.5 FILLAUER LLC (UNITED STATES)

7.6 WILLOWWOOD GLOBAL LLC (UNITED STATES)

7.7 STEEPER GROUP (UNITED KINGDOM)

7.8 HANGER INC. (UNITED STATES)

7.9 PROTEOR (FRANCE)

7.10 TRULIFE (IRELAND)

7.11 RSL STEEPER (UNITED KINGDOM)

7.12 OHIO WILLOW WOOD (UNITED STATES)

7.13 ZIMMER BIOMET (UNITED STATES)

7.14 OTHER ACTIVE PLAYERS

Chapter 8: Global Orthopedic Prosthetic Market By Region

8.1 Overview

8.2. North America Orthopedic Prosthetic Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size By Product Type

8.2.4.1 Upper Extremity Prosthetics

8.2.4.2 Lower Extremity Prosthetics

8.2.4.3 Socket Prosthetics

8.2.4.4 Modular Components

8.2.5 Historic and Forecasted Market Size By Technology

8.2.5.1 Conventional Prosthetics

8.2.5.2 Electric-powered Prosthetics

8.2.5.3 Hybrid Prosthetics

8.2.6 Historic and Forecasted Market Size By End User

8.2.6.1 Hospitals

8.2.6.2 Prosthetic Clinics

8.2.6.3 Rehabilitation Centers

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Orthopedic Prosthetic Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size By Product Type

8.3.4.1 Upper Extremity Prosthetics

8.3.4.2 Lower Extremity Prosthetics

8.3.4.3 Socket Prosthetics

8.3.4.4 Modular Components

8.3.5 Historic and Forecasted Market Size By Technology

8.3.5.1 Conventional Prosthetics

8.3.5.2 Electric-powered Prosthetics

8.3.5.3 Hybrid Prosthetics

8.3.6 Historic and Forecasted Market Size By End User

8.3.6.1 Hospitals

8.3.6.2 Prosthetic Clinics

8.3.6.3 Rehabilitation Centers

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Orthopedic Prosthetic Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size By Product Type

8.4.4.1 Upper Extremity Prosthetics

8.4.4.2 Lower Extremity Prosthetics

8.4.4.3 Socket Prosthetics

8.4.4.4 Modular Components

8.4.5 Historic and Forecasted Market Size By Technology

8.4.5.1 Conventional Prosthetics

8.4.5.2 Electric-powered Prosthetics

8.4.5.3 Hybrid Prosthetics

8.4.6 Historic and Forecasted Market Size By End User

8.4.6.1 Hospitals

8.4.6.2 Prosthetic Clinics

8.4.6.3 Rehabilitation Centers

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Orthopedic Prosthetic Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size By Product Type

8.5.4.1 Upper Extremity Prosthetics

8.5.4.2 Lower Extremity Prosthetics

8.5.4.3 Socket Prosthetics

8.5.4.4 Modular Components

8.5.5 Historic and Forecasted Market Size By Technology

8.5.5.1 Conventional Prosthetics

8.5.5.2 Electric-powered Prosthetics

8.5.5.3 Hybrid Prosthetics

8.5.6 Historic and Forecasted Market Size By End User

8.5.6.1 Hospitals

8.5.6.2 Prosthetic Clinics

8.5.6.3 Rehabilitation Centers

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Orthopedic Prosthetic Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size By Product Type

8.6.4.1 Upper Extremity Prosthetics

8.6.4.2 Lower Extremity Prosthetics

8.6.4.3 Socket Prosthetics

8.6.4.4 Modular Components

8.6.5 Historic and Forecasted Market Size By Technology

8.6.5.1 Conventional Prosthetics

8.6.5.2 Electric-powered Prosthetics

8.6.5.3 Hybrid Prosthetics

8.6.6 Historic and Forecasted Market Size By End User

8.6.6.1 Hospitals

8.6.6.2 Prosthetic Clinics

8.6.6.3 Rehabilitation Centers

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Orthopedic Prosthetic Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size By Product Type

8.7.4.1 Upper Extremity Prosthetics

8.7.4.2 Lower Extremity Prosthetics

8.7.4.3 Socket Prosthetics

8.7.4.4 Modular Components

8.7.5 Historic and Forecasted Market Size By Technology

8.7.5.1 Conventional Prosthetics

8.7.5.2 Electric-powered Prosthetics

8.7.5.3 Hybrid Prosthetics

8.7.6 Historic and Forecasted Market Size By End User

8.7.6.1 Hospitals

8.7.6.2 Prosthetic Clinics

8.7.6.3 Rehabilitation Centers

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

Q1: What would be the forecast period in the Orthopedic Prosthetic Market research report?

A1: The forecast period in the Orthopedic Prosthetic Market research report is 2024-2032.

Q2: Who are the key players in the Orthopedic Prosthetic Market?

A2: Aether Biomedical (Poland), BioMetrics Prosthetic and Orthotic Group (USA), Bionic Prosthetics and Orthotics Group (USA), Blatchford Ltd. (UK), College Park Industries (USA), Endolite India Ltd. (India), Exoneural Network AB (Sweden), Fillauer LLC (USA), Freedom Innovations (USA), Medi Prosthetics (India), Motion Control Inc. (USA), Össur (Iceland), Ottobock (Germany), Protunix (USA), Reboocon Bionics (Netherlands), RSLSteeper (UK), Spinal Technology Inc. (USA), Steeper Group (UK), Trulife (Ireland), WillowWood Global LLC (USA), and Other Active Players.

Q3: What are the segments of the Orthopedic Prosthetic Market?

A3: The Orthopedic Prosthetic Market is segmented into Product Type, Technology, End User and region. By Product Type, the market is categorized into Upper Extremity Prosthetics, Lower Extremity Prosthetics, Socket Prosthetics, Modular Components. By Technology, the market is categorized into Conventional Prosthetics, Electric-powered Prosthetics, Hybrid Prosthetics. By End User, the market is categorized into Hospitals, Prosthetic Clinics, Rehabilitation Centers. By region, it is analyzed across North America (U.S., Canada, Mexico), Eastern Europe (Russia, Bulgaria, The Czech Republic, Hungary, Poland, Romania, Rest of Eastern Europe), Western Europe (Germany, UK, France, Netherlands, Italy, Spain, Rest of Western Europe), Asia Pacific (China, India, Japan, South Korea, Malaysia, Thailand, Vietnam, The Philippines, Australia, New-Zealand, Rest of APAC), Middle East & Africa (Türkiye, Bahrain, Kuwait, Saudi Arabia, Qatar, UAE, Israel, South Africa), South America (Brazil, Argentina, Rest of SA).

Q4: What is the Orthopedic Prosthetic Market?

A4: The Orthopedic Prosthetic Market is the branch of the health care industry charged with the responsibility of providing artificial limbs and other orthopedic supportive equipment to patients who have lost limbs through accidents, diseases and genetic factors. This market plays a crucial role in making patients regain their mobility and functionality, besides improving their quality of life using technology.

Q5: How big is the Orthopedic Prosthetic Market?

A5: Orthopedic Prosthetic Market Size Was Valued at USD 6.6 Billion in 2023, and is Projected to Reach USD 11.1 Billion by 2032, Growing at a CAGR of 5.92% From 2024-2032.

How to Buy a Report from eminsights.jp

On the product page, choose the license you want: Single-User License, Multi-User License or Enterprise License.

If you required report in your native language, then you can click on Translated Report button and fill out the form with report name and language you want, then our team will contact you as soon as possible.

Click the Buy Now button.

You will be redirected to the checkout page. Enter your company details and payment information.

Click Place Order to complete the purchase.

Confirmation: You’ll receive an order confirmation and our team will contact you shortly with your ordered report.

If you have any questions, fill out the contact form below or email us at bizdev@eminsights.net.

Thank you for choosing eminsights.jp!