Stay Ahead in Fast-Growing Economies.

Browse Reports Now

Electric Vehicle (EV) Charging Equipment Market- Global Industry Growth and Trend Analysis

EV charging equipment is an electronic device that provides electric energy from a power source to recharge an electric vehicle, such as a plug-in electric vehicle such as a passenger electric car or a light commercial vehicle. Furthermore, EV Charging equipment serves as a vital link between an electrical source and an electric vehicle with depleted battery power. EV charging equipment is typically in the form of a fixture that is directly connected to an electrical distribution panel or, in some cases, an electrical outlet.

IMR Group

Description

Electric Vehicle (EV) Charging Equipment Market Synopsis

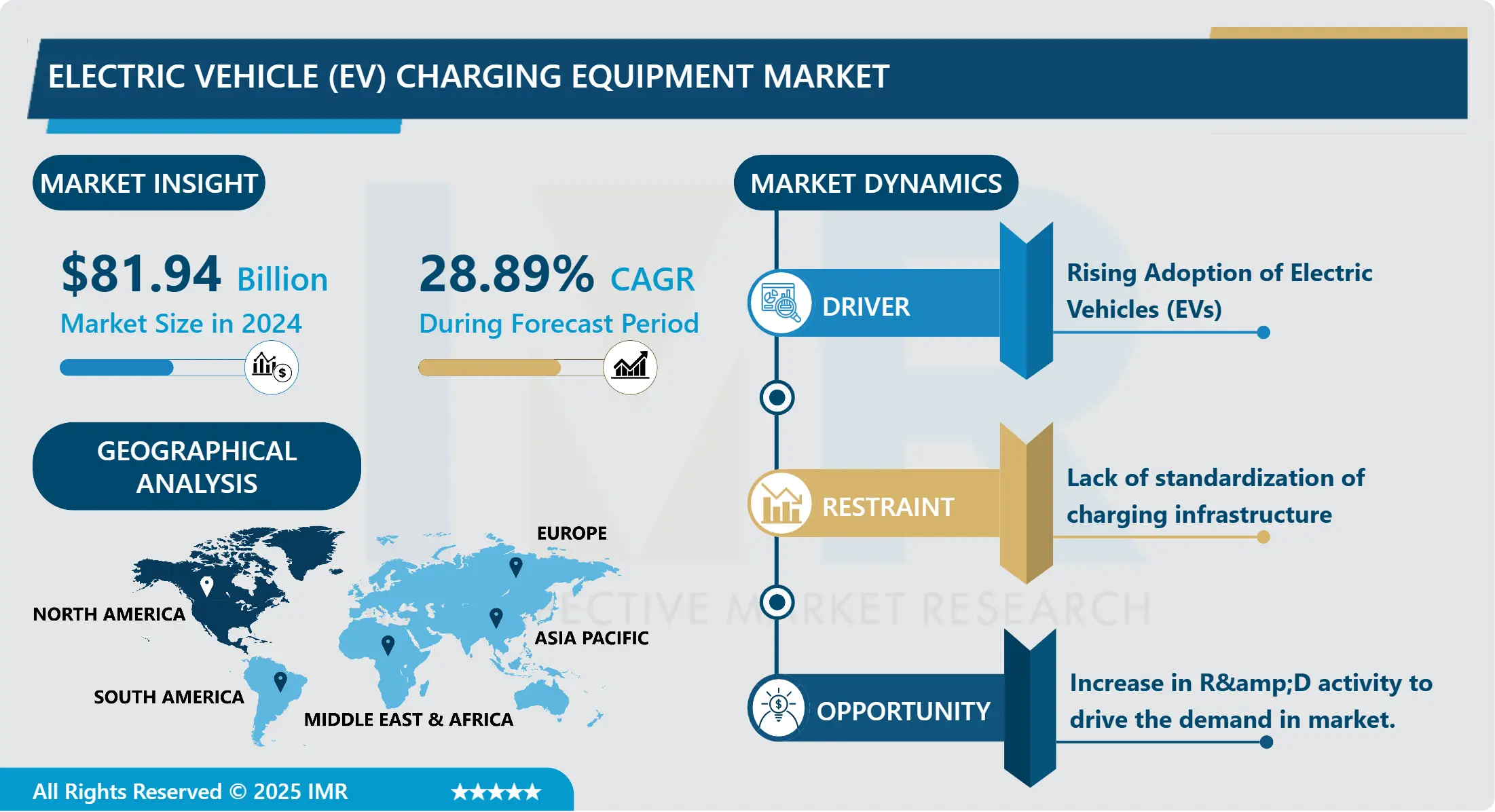

Electric Vehicle (EV) Charging Equipment Market Size Was Valued at USD 81.94 Billion in 2024, and is Projected to Reach USD 624.09 Billion by 2032, Growing at a CAGR of 28.89% From 2025-2032.

In recent years, the electric vehicle (EV) charging equipment market has expanded significantly, propelled by the worldwide trend toward environmentally friendly modes of transportation. In response to growing apprehensions regarding air pollution and climate change, governments across the globe have been enacting policies and providing incentives to promote the use of electric vehicles. There has been an increase in demand for various types of electric vehicle (EV) charging infrastructure, including fast-charging stations along highways, public charging networks, and residential charging stations.

We anticipate continuous expansion of the EV charging equipment market as automakers further integrate electric vehicles into their lineup and battery technology advances. This development will create profitable prospects for manufacturers, service providers, and investors in the market.

The market overview reveals a highly competitive environment characterized by strategic alliances and technological advancements in the ever-evolving business climate. Industry leaders in electric vehicle (EV) charging equipment invest consistently in research and development to optimize charging processes, decrease charging durations, and enhance the overall user experience.

Furthermore, there is a growing trend of partnerships among energy companies, automotive manufacturers, and charging infrastructure providers. The objective is to create all-encompassing charging ecosystems that tackle obstacles associated with grid integration and interoperability.

The development of innovative solutions and the expansion of charging infrastructure will be pivotal in enabling widespread adoption and maximizing the potential of electric mobility as the EV market continues to mature and develop.

Electric Vehicle (EV) Charging Equipment Market Trend Analysis

Expansion of fast-charging networks

The market for electric vehicle (EV) charging equipment is currently undergoing a substantial upward trajectory, propelled by the exponential expansion of electric vehicles on a global scale. The growing adoption of electric vehicles (EVs) by consumers has resulted in an intensified need for charging infrastructure. This phenomenon is notable for the proliferation of fast-charging infrastructure.

Fast-charging networks provide EV drivers with convenient and expedient charging options, making them vital for addressing range anxiety. Government initiatives promoting sustainable transportation, technological advancements in charging, and the efforts of key industry participants to construct a robust charging infrastructure all contribute to this growth.

Furthermore, the increasing use of electric vehicles by ridesharing companies and fleet operators underscores the importance of rapid charging infrastructure to ensure the efficient functioning of these businesses. In addition to improving the ease of owning electric vehicles, these networks also aid in the reduction of greenhouse gas emissions and reliance on fossil fuels.

In order to take advantage of this increasing need, participants in the electric vehicle ecosystem are making substantial investments in the installation of rapid-charging stations in commercial centers, highways, and urban regions. Moreover, partnerships among energy companies, automakers, and providers of charging infrastructure are promoting standardization and innovation in charging technology, thereby enhancing the accessibility and dependability of rapid charging for electric vehicle (EV) users.

We anticipate that the proliferation of fast-charging infrastructure will significantly influence the trajectory of the electric vehicle industry, promoting widespread acceptance and facilitating the shift towards environmentally friendly modes of transportation.

Integration of Smart Charging Technologies

The market for electric vehicle (EV) charging equipment is currently undergoing significant expansion, propelled by the global surge in EV adoption. The transition towards sustainable transportation solutions and government initiatives that encourage the adoption of electric vehicles significantly propel market expansion.

Intelligent charging technologies are an emerging phenomenon in the electric vehicle (EV) charging apparatus market. These technologies facilitate smart charging procedures by enabling electric vehicles (EVs) to establish communication with charging stations. Consequently, these technologies optimize charging schedules by considering variables like electricity rates, grid demand, and vehicle utilization patterns. In addition to promoting grid integration, intelligent charging solutions assist in balancing electricity supply and demand, thereby reducing grid strain during peak hours.

In addition, progress in connectivity and data analytics has facilitated the creation of intelligent charging infrastructure, which provides remote monitoring, payment processing, and user authentication, among other capabilities. These functionalities boost operational efficiency, facilitate the expansion of electric vehicle fleets in both commercial and residential environments, and enhance the overall user experience.

The implementation of intelligent charging technologies will be pivotal in bolstering the dependability, scalability, and sustainability of charging infrastructure as the electric vehicle (EV) market continues to expand. This, in turn, will stimulate additional advancements and market expansion.

Electric Vehicle (EV) Charging Equipment Segment Analysis:

Electric Vehicle (EV) Charging Equipment Market Segmented based on Charging Station Type, Power Output, Component, Supplier Type, End User, and Region.

Public Charging Stations is Dominate the Electric Vehicle (EV) Charging Equipment market

The market for charging apparatus for electric vehicles (EVs) is undergoing change, as evidenced by the emergence of distinct trends in public and residential charging stations.

The rapid expansion of public charging stations is the result of rising EV adoption and government initiatives to promote the development of public charging infrastructure. These charging stations frequently integrate sophisticated functionalities, including payment systems and rapid charging capabilities, to accommodate the requirements of electric vehicle owners who are constantly on the move.

Conversely, residential charging stations are gaining traction among EV owners in search of economical and convenient charging alternatives. Typically situated in residential areas, these stations provide the added benefit of overnight charging, guaranteeing that electric vehicles are prepared for daily operation.

The public and residential charging segments of the EV charging equipment market are expanding at a rate consistent with the rising demand for electric vehicles and the development of charging infrastructure to facilitate their widespread adoption.

Power Output Segment is anticipated to maintain market share over the forecast period.

The Electric Vehicle (EV) charging equipment market is segmented based on power output into three main categories: Level 1, Level 2, and Level 3 charging stations.

Level 1 charging stations typically provide power outputs up to 7.2 kW and are commonly used for residential charging. These stations are often plugged into standard household outlets and offer convenient slow charging options, suitable for overnight charging needs.

Level 2 charging stations offer power outputs ranging from 7.2 kW to 22 kW, catering to both residential and commercial charging needs. These stations provide faster charging compared to Level 1, making them suitable for home charging as well as public and workplace installations.

Level 3 charging stations, also known as DC fast chargers, deliver power outputs above 22 kW, enabling rapid charging for EVs. These stations are primarily deployed in high-traffic areas and along highways to support long-distance travel and reduce charging time for drivers, thus promoting the widespread adoption of electric vehicles.

Global Electric Vehicle (EV) Charging Equipment Market Regional Insights

North America has witnessed substantial growth in Electric Vehicle (EV) Charging Equipment market

The electric vehicle (EV) charging infrastructure in North America has expanded substantially due to a number of factors, including rising consumer demand, environmental consciousness, and government incentives.

Subsidies, tax credits, and grants have provided incentives for the installation of electric vehicle (EV) charging stations throughout the region, with a particular focus on urban areas and key transportation corridors.

This expansion of EV charging infrastructure in North America has stimulated the growth of the electric vehicle (EV) charging equipment market. There is a growing trend among market participants to allocate resources towards research and development endeavors that aim to introduce novel charging technologies, augment charging velocities, and elevate the overall user experience.

Furthermore, collaborations among technology companies, utilities, automotive manufacturers, and utilities are expediting charging infrastructure installation and fostering interoperability among diverse charging networks. Manufacturers and service providers of EV charging equipment anticipate North America to remain a pivotal region as the EV market continues to expand.

Active Key Players in the Electric Vehicle (EV) Charging Equipment Market

Tesla, Inc. (United States)

ChargePoint, Inc. (United States)

EVBox Group (Netherlands)

ABB Ltd. (Switzerland)

Schneider Electric SE (France)

Siemens AG (Germany)

Blink Charging Co.(United States)

Engie SA(France)

EVgo Services LLC (United States)

Allego B.V. (Netherlands)

Tritium Pty Ltd (Australia)

Leviton Manufacturing Co., Inc. (United States)

Efacec Electric Mobility, S.A. (Portugal)

AeroVironment, Inc. (United States)

Webasto Group (Germany)

ClipperCreek, Inc. (United States)

Delta Electronics, Inc. (Taiwan)

GARO AB (Sweden)

SemaConnect, Inc.(United States)

Other Active Players

Key Industry Developments in the Electric Vehicle (EV) Charging Equipment Market:

In August 2024, Wallbox Chargers, a company specializing in the design, manufacturing, and distribution of EV charging systems, and ChargeLab, an EV charging software provider, recently announced a partnership aimed at simplifying commercial EV charger deployments. The alliance, which focused on deployments across North America, integrated Wallbox hardware and ChargeLab software into a bundled offering for electrical distributors. This collaboration sought to streamline and enhance the overall experience for distributors. Fred Turner, a Senior Director at Wallbox, highlighted the importance of this partnership in achieving greater efficiency and ease of use for commercial EV charger installations.

In June 2024, Exicom Tele-Systems Limited, India’s largest electric vehicle (EV) charger manufacturer, recently acquired Tritium, a prominent DC fast charger manufacturer, for up to $29.63 million. This strategic move reflects Exicom’s commitment to expanding its global footprint in the EV charger market. By acquiring Tritium’s business and assets, Exicom has bolstered its position in the international EV charging industry, further solidifying its influence. The acquisition marks a significant step in Exicom’s growth strategy, enabling it to enhance its global presence and compete more effectively in the rapidly evolving EV market.

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter’s Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Electric Vehicle (EV) Charging Equipment Market by Charging Station Type (2018-2032)

4.1 Electric Vehicle (EV) Charging Equipment Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Public charging stations

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Home Charging Stations

Chapter 5: Electric Vehicle (EV) Charging Equipment Market by Power Output (2018-2032)

5.1 Electric Vehicle (EV) Charging Equipment Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Level 1 (up to 7.2 kW)

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Level 2 (7.2 kW–22 kW)

5.5 Level 3 (above 22 kW)

Chapter 6: Electric Vehicle (EV) Charging Equipment Market by Component (2018-2032)

6.1 Electric Vehicle (EV) Charging Equipment Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Hardware

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Software

Chapter 7: Electric Vehicle (EV) Charging Equipment Market by Supplier Type (2018-2032)

7.1 Electric Vehicle (EV) Charging Equipment Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Original Equipment Manufacturers (OEMs)

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Independent Charging Infrastructure Providers

Chapter 8: Electric Vehicle (EV) Charging Equipment Market by End User (2018-2032)

8.1 Electric Vehicle (EV) Charging Equipment Market Snapshot and Growth Engine

8.2 Market Overview

8.3 Commercial

8.3.1 Introduction and Market Overview

8.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

8.3.3 Key Market Trends, Growth Factors, and Opportunities

8.3.4 Geographic Segmentation Analysis

8.4 Residential

Chapter 9: Company Profiles and Competitive Analysis

9.1 Competitive Landscape

9.1.1 Competitive Benchmarking

9.1.2 Electric Vehicle (EV) Charging Equipment Market Share by Manufacturer (2024)

9.1.3 Industry BCG Matrix

9.1.4 Heat Map Analysis

9.1.5 Mergers and Acquisitions

9.2 EXXON MOBIL CORPORATION

9.2.1 Company Overview

9.2.2 Key Executives

9.2.3 Company Snapshot

9.2.4 Role of the Company in the Market

9.2.5 Sustainability and Social Responsibility

9.2.6 Operating Business Segments

9.2.7 Product Portfolio

9.2.8 Business Performance

9.2.9 Key Strategic Moves and Recent Developments

9.2.10 SWOT Analysis

9.3 TOTAL ENERGIES

9.4 SHELL PLC

9.5 FUCHS

9.6 BP P.L.C.

9.7 ROYAL DUTCH SHELL PLC

9.8 FUCHS PETROLUB AG

9.9 PETRONAS

9.10 ENEOS CORPORATION

9.11 REPSOL S.A.

9.12 VALVOLINE INC.

9.13 PTT

9.14 PETROLIAM NASIONAL BERHAD (PETRONAS)

9.15 SAUDI ARABIAN OIL COOTHER KEY PLAYERS

Chapter 10: Global Electric Vehicle (EV) Charging Equipment Market By Region

10.1 Overview

10.2. North America Electric Vehicle (EV) Charging Equipment Market

10.2.1 Key Market Trends, Growth Factors and Opportunities

10.2.2 Top Key Companies

10.2.3 Historic and Forecasted Market Size by Segments

10.2.4 Historic and Forecasted Market Size by Charging Station Type

10.2.4.1 Public charging stations

10.2.4.2 Home Charging Stations

10.2.5 Historic and Forecasted Market Size by Power Output

10.2.5.1 Level 1 (up to 7.2 kW)

10.2.5.2 Level 2 (7.2 kW–22 kW)

10.2.5.3 Level 3 (above 22 kW)

10.2.6 Historic and Forecasted Market Size by Component

10.2.6.1 Hardware

10.2.6.2 Software

10.2.7 Historic and Forecasted Market Size by Supplier Type

10.2.7.1 Original Equipment Manufacturers (OEMs)

10.2.7.2 Independent Charging Infrastructure Providers

10.2.8 Historic and Forecasted Market Size by End User

10.2.8.1 Commercial

10.2.8.2 Residential

10.2.9 Historic and Forecast Market Size by Country

10.2.9.1 US

10.2.9.2 Canada

10.2.9.3 Mexico

10.3. Eastern Europe Electric Vehicle (EV) Charging Equipment Market

10.3.1 Key Market Trends, Growth Factors and Opportunities

10.3.2 Top Key Companies

10.3.3 Historic and Forecasted Market Size by Segments

10.3.4 Historic and Forecasted Market Size by Charging Station Type

10.3.4.1 Public charging stations

10.3.4.2 Home Charging Stations

10.3.5 Historic and Forecasted Market Size by Power Output

10.3.5.1 Level 1 (up to 7.2 kW)

10.3.5.2 Level 2 (7.2 kW–22 kW)

10.3.5.3 Level 3 (above 22 kW)

10.3.6 Historic and Forecasted Market Size by Component

10.3.6.1 Hardware

10.3.6.2 Software

10.3.7 Historic and Forecasted Market Size by Supplier Type

10.3.7.1 Original Equipment Manufacturers (OEMs)

10.3.7.2 Independent Charging Infrastructure Providers

10.3.8 Historic and Forecasted Market Size by End User

10.3.8.1 Commercial

10.3.8.2 Residential

10.3.9 Historic and Forecast Market Size by Country

10.3.9.1 Russia

10.3.9.2 Bulgaria

10.3.9.3 The Czech Republic

10.3.9.4 Hungary

10.3.9.5 Poland

10.3.9.6 Romania

10.3.9.7 Rest of Eastern Europe

10.4. Western Europe Electric Vehicle (EV) Charging Equipment Market

10.4.1 Key Market Trends, Growth Factors and Opportunities

10.4.2 Top Key Companies

10.4.3 Historic and Forecasted Market Size by Segments

10.4.4 Historic and Forecasted Market Size by Charging Station Type

10.4.4.1 Public charging stations

10.4.4.2 Home Charging Stations

10.4.5 Historic and Forecasted Market Size by Power Output

10.4.5.1 Level 1 (up to 7.2 kW)

10.4.5.2 Level 2 (7.2 kW–22 kW)

10.4.5.3 Level 3 (above 22 kW)

10.4.6 Historic and Forecasted Market Size by Component

10.4.6.1 Hardware

10.4.6.2 Software

10.4.7 Historic and Forecasted Market Size by Supplier Type

10.4.7.1 Original Equipment Manufacturers (OEMs)

10.4.7.2 Independent Charging Infrastructure Providers

10.4.8 Historic and Forecasted Market Size by End User

10.4.8.1 Commercial

10.4.8.2 Residential

10.4.9 Historic and Forecast Market Size by Country

10.4.9.1 Germany

10.4.9.2 UK

10.4.9.3 France

10.4.9.4 The Netherlands

10.4.9.5 Italy

10.4.9.6 Spain

10.4.9.7 Rest of Western Europe

10.5. Asia Pacific Electric Vehicle (EV) Charging Equipment Market

10.5.1 Key Market Trends, Growth Factors and Opportunities

10.5.2 Top Key Companies

10.5.3 Historic and Forecasted Market Size by Segments

10.5.4 Historic and Forecasted Market Size by Charging Station Type

10.5.4.1 Public charging stations

10.5.4.2 Home Charging Stations

10.5.5 Historic and Forecasted Market Size by Power Output

10.5.5.1 Level 1 (up to 7.2 kW)

10.5.5.2 Level 2 (7.2 kW–22 kW)

10.5.5.3 Level 3 (above 22 kW)

10.5.6 Historic and Forecasted Market Size by Component

10.5.6.1 Hardware

10.5.6.2 Software

10.5.7 Historic and Forecasted Market Size by Supplier Type

10.5.7.1 Original Equipment Manufacturers (OEMs)

10.5.7.2 Independent Charging Infrastructure Providers

10.5.8 Historic and Forecasted Market Size by End User

10.5.8.1 Commercial

10.5.8.2 Residential

10.5.9 Historic and Forecast Market Size by Country

10.5.9.1 China

10.5.9.2 India

10.5.9.3 Japan

10.5.9.4 South Korea

10.5.9.5 Malaysia

10.5.9.6 Thailand

10.5.9.7 Vietnam

10.5.9.8 The Philippines

10.5.9.9 Australia

10.5.9.10 New Zealand

10.5.9.11 Rest of APAC

10.6. Middle East & Africa Electric Vehicle (EV) Charging Equipment Market

10.6.1 Key Market Trends, Growth Factors and Opportunities

10.6.2 Top Key Companies

10.6.3 Historic and Forecasted Market Size by Segments

10.6.4 Historic and Forecasted Market Size by Charging Station Type

10.6.4.1 Public charging stations

10.6.4.2 Home Charging Stations

10.6.5 Historic and Forecasted Market Size by Power Output

10.6.5.1 Level 1 (up to 7.2 kW)

10.6.5.2 Level 2 (7.2 kW–22 kW)

10.6.5.3 Level 3 (above 22 kW)

10.6.6 Historic and Forecasted Market Size by Component

10.6.6.1 Hardware

10.6.6.2 Software

10.6.7 Historic and Forecasted Market Size by Supplier Type

10.6.7.1 Original Equipment Manufacturers (OEMs)

10.6.7.2 Independent Charging Infrastructure Providers

10.6.8 Historic and Forecasted Market Size by End User

10.6.8.1 Commercial

10.6.8.2 Residential

10.6.9 Historic and Forecast Market Size by Country

10.6.9.1 Turkiye

10.6.9.2 Bahrain

10.6.9.3 Kuwait

10.6.9.4 Saudi Arabia

10.6.9.5 Qatar

10.6.9.6 UAE

10.6.9.7 Israel

10.6.9.8 South Africa

10.7. South America Electric Vehicle (EV) Charging Equipment Market

10.7.1 Key Market Trends, Growth Factors and Opportunities

10.7.2 Top Key Companies

10.7.3 Historic and Forecasted Market Size by Segments

10.7.4 Historic and Forecasted Market Size by Charging Station Type

10.7.4.1 Public charging stations

10.7.4.2 Home Charging Stations

10.7.5 Historic and Forecasted Market Size by Power Output

10.7.5.1 Level 1 (up to 7.2 kW)

10.7.5.2 Level 2 (7.2 kW–22 kW)

10.7.5.3 Level 3 (above 22 kW)

10.7.6 Historic and Forecasted Market Size by Component

10.7.6.1 Hardware

10.7.6.2 Software

10.7.7 Historic and Forecasted Market Size by Supplier Type

10.7.7.1 Original Equipment Manufacturers (OEMs)

10.7.7.2 Independent Charging Infrastructure Providers

10.7.8 Historic and Forecasted Market Size by End User

10.7.8.1 Commercial

10.7.8.2 Residential

10.7.9 Historic and Forecast Market Size by Country

10.7.9.1 Brazil

10.7.9.2 Argentina

10.7.9.3 Rest of SA

Chapter 11 Analyst Viewpoint and Conclusion

11.1 Recommendations and Concluding Analysis

11.2 Potential Market Strategies

Chapter 12 Research Methodology

12.1 Research Process

12.2 Primary Research

12.3 Secondary Research

Q1: What would be the forecast period in the Electric Vehicle (EV) Charging Equipment Market research report?

A1: The forecast period in the Electric Vehicle (EV) Charging Equipment Market research report is 2025-2032.

Q2: Who are the key players in the Electric Vehicle (EV) Charging Equipment Market?

A2: Tesla, Inc. (United States),ChargePoint, Inc. (United States),EVBox Group (Netherlands),ABB Ltd. (Switzerland),Schneider Electric SE (France),Siemens AG (Germany),Blink Charging Co.(United States),Engie SA(France),EVgo Services LLC (United States),Allego B.V. (Netherlands),Tritium Pty Ltd (Australia),Leviton Manufacturing Co., Inc. (United States),Efacec Electric Mobility, S.A. (Portugal),AeroVironment, Inc. (United States),Webasto Group (Germany),ClipperCreek, Inc. (United States),Delta Electronics, Inc. (Taiwan),GARO AB (Sweden),SemaConnect, Inc.(United States), and Other Active Players

Q3: What are the segments of Electric Vehicle (EV) Charging Equipment Market?

A3: The Electric Vehicle (EV) Charging Equipment Market is segmented into Charging Station Type, Power Output, Component, Supplier Type, End User, and Region. By Charging Station Type, the market is categorized into Public charging stations, Home Charging Stations. By Power Output, the market is categorized into Level 1 (up to 7.2 kW), Level 2 (7.2 kW–22 kW), Level 3 (above 22 kW. By Component, the market is categorized into Hardware and Software. By Supplier Type, the market is categorized into Original Equipment Manufacturers (OEMs), Independent Charging Infrastructure Providers. By End User, the market is categorized into Commercial, Residential. By Region, it is analyzed across North America (U.S.; Canada; Mexico), Eastern Europe (Russia; Bulgaria; The Czech Republic; Hungary; Poland; Romania; Rest of Eastern Europe), Western Europe (Germany; UK; France; The Netherlands; Italy; ; Spain; Rest of Western Europe), Asia-Pacific (China, India, Japan, South Korea, Malaysia, Thailand, Vietnam, The Philippines, Australia, New Zealand, Rest of APAC), Middle East & Africa (Türkiye, Bahrain, Kuwait, Saudi Arabia, Qatar, UAE, Israel, South Africa), South America (Brazil; Argentina, Rest of SA.).

Q4: What is the Electric Vehicle (EV) Charging Equipment Market?

A4: The electric vehicle (EV) charging apparatus market refers to the sector that manufactures and distributes the necessary infrastructure for EV charging. The increasing global adoption of electric vehicles has led to a corresponding surge in the demand for charging stations and associated equipment. This market comprises charging stations, charging cables, connectors, and software and hardware solutions that are associated with them. In response to the expanding fleet of electric vehicles and rising environmental concerns, governments and private organizations are making substantial investments in the expansion of EV charging infrastructure. Government incentives, the demand for environmentally friendly transportation, and the ongoing development of charging technologies that reduce charging times and increase efficacy all have an impact on the market. Moreover, the proliferation of electric vehicles in various sectors—including private automobiles, commercial vehicles, and public transportation—contributes to the expansion of the market for EV charging equipment.

Q5: How big is the Electric Vehicle (EV) Charging Equipment Market?

A5: Electric Vehicle (EV) Charging Equipment Market Size Was Valued at USD 81.94 Billion in 2024, and is Projected to Reach USD 624.09 Billion by 2032, Growing at a CAGR of 28.89% From 2025-2032.

How to Buy a Report from eminsights.jp

On the product page, choose the license you want: Single-User License, Multi-User License or Enterprise License.

If you required report in your native language, then you can click on Translated Report button and fill out the form with report name and language you want, then our team will contact you as soon as possible.

Click the Buy Now button.

You will be redirected to the checkout page. Enter your company details and payment information.

Click Place Order to complete the purchase.

Confirmation: You’ll receive an order confirmation and our team will contact you shortly with your ordered report.

If you have any questions, fill out the contact form below or email us at bizdev@eminsights.net.

Thank you for choosing eminsights.jp!